The main goal of a circular economy model is to produce goods and services in a sustainable manner by reducing the consumption and waste of resources (raw materials, water, energy). It contradicts with the traditional linear economy, that of a ‘take-make-consume-waste’.

According to many, a circular economy requires a local production capacity. It is a process that depends on fundamental changes to the existing production and consumption systems. According to the World Economic Forum, the world’s economy is only 9% circular. To become more efficient and preserve our natural resources, we must open our eyes and begin to think circular rather than linear.

Today, we are going to focus on the Circular Economy model, its principles, benefits, and existing solutions implemented to tackle the traditional linear economy.

The principles of the Circular Economy

In this model, every single product is manufactured and designed for future reuse, and ideally, at the end of its lifetime, it becomes a potential resource. Within this model, each stage in the economic cycle is modified, from producing goods and services to using them. It is an environment where products are built to last, with less energy and resources consumed. Please find below the three main principles of the Circular Economy.

1. Design out waste and pollution

What if waste and pollution were never created in the first place? In a circular model, product waste is eliminated straight from the design stage, meaning that goods can be used and reused longer, fixed more easily, and finally recycled to create additional industrial inputs.

2. Keep products and materials in use

A circular economy promotes activities where value in terms of energy, labor, and material is preserved. With the available technologies and innovative solutions, products should be designed for durability, reuse, remanufacturing, and recycling. This leads to a closed-loop production system, where components are circulating the economy. It takes advantage of bio-based materials, allowing businesses to reuse them for several products.

3. Regenerate natural systems

The process of extracting and processing natural resources causes 90% of global biodiversity loss and water stress while harming the global climate. The World Economic Forum predicts that by 2060, the current resource use of 190 billion tones will double and exceed our planetary boundaries. Therefore, changes in business and policy models must occur.

A circular economy is designed to eliminate the use of non-renewable resources, preserving, and focusing on renewable ones. This way, valuable nutrients are returned to the soil and renewable energy is used rather than fossil fuels.

Economic benefits of a Circular Economy

At a macro level, circularity has many economic advantages. A surplus of $2 trillion a year could result from more effective resource management. This is due to a substantial decrease in the cost of raw materials.

- Considerable resource savings

Even if more and more people become aware of the circular economy model, the extraction and prices of the main raw materials are still on the rise. In 2019, only 9% of all raw materials were recycled. In theory, a circular economy should recycle 100% of these materials, without new virgin raw materials required. However, it is predicted that this scenario will take quite a long time to be accomplished. Innovative methods should be applied to completely recycle materials that are utilized in production.

- Economic growth

In this model, economic growth is not dependent on the scarcity of raw materials. It is predicted that a shift towards the circular economy is set to promote economic growth. Since new raw materials are not extracted anymore, the development, maintenance, and production of circular products will require a specialized workforce, increasing the number of jobs. With less demand for specialized jobs in the extraction and processing of raw materials, specialized employees will have to adjust to a new work environment.

- Employment opportunities

As previously mentioned, the need to extract raw materials is not fundamental within a circular model. For this reason, such an economy requires a specialized workforce with a new set of relevant skills and aptitudes. Therefore, workers that extract and process raw materials might have to adapt and get familiar with new procedures and environments. The existing studies anticipate a modest, but positive impact of Circular Economy on employment volume.

- A good reason to innovate

Change comes with a desire to innovate. Thinking circular rather than linear already motivates innovators to optimize the entire system. This will form new collaborations between different parties involved, such as recyclers, producers, and designers. They can add more knowledge and great value in terms of sustainable innovations.

Circular Economy solutions

- CleanCup

Headquartered in Lyon, France, CleanCup is a solution designed to eliminate the use of disposable cups. They promote it as a turnkey solution meant to distribute, collect, and automatically wash reusable cups. Places such as campuses, companies, and communities are prioritized since those tend to generate a lot of waste.

Globally, it was established that people use 500 billion plastic cups and 16 billion coffee cups coated in paper. In theory, it is possible to recycle disposable cups, but the manufacturing process tends to be somewhat difficult, leading to very few of them being recycled. With CleanCup, one can get a clean and empty cup for a 1€ deposit. At any point in time, the user simply puts the cup back inside the machine and gets back the deposit. As soon as a cup is returned, the machine automatically washes it to be reused.

- Positive Energy Ltd.

This is a matchmaking platform between investors and small to mid-scale renewable energy facilities. Its purpose is to allow investors to easily find projects that require renewable energy financing. This blockchain-based asset financing, trading, and management platform digitalize the transaction workflow, making renewable energy investments fast, liquid, and transparent for all parties involved.

This initiative aims to boost renewable energy investments. By 2030, it could save around 20 million tons of CO2 per year. It is widely accessible and profitable for shareholders, with return on investment.

- RePack

This solution replaces the single-use delivery packages in e-commerce, providing reusable, and returnable delivery packaging. It is cost-efficient and environmentally friendly, with 78% less CO2 created and 92% less landfill waste, compared to traditional packaging.

Users can simply return these packages in letter-size or to any location using RePack packaging. Customers are incentivized to return used boxes through different vouchers to be redeemed at any participating RePack store. This packaging can be used at least 20 times.

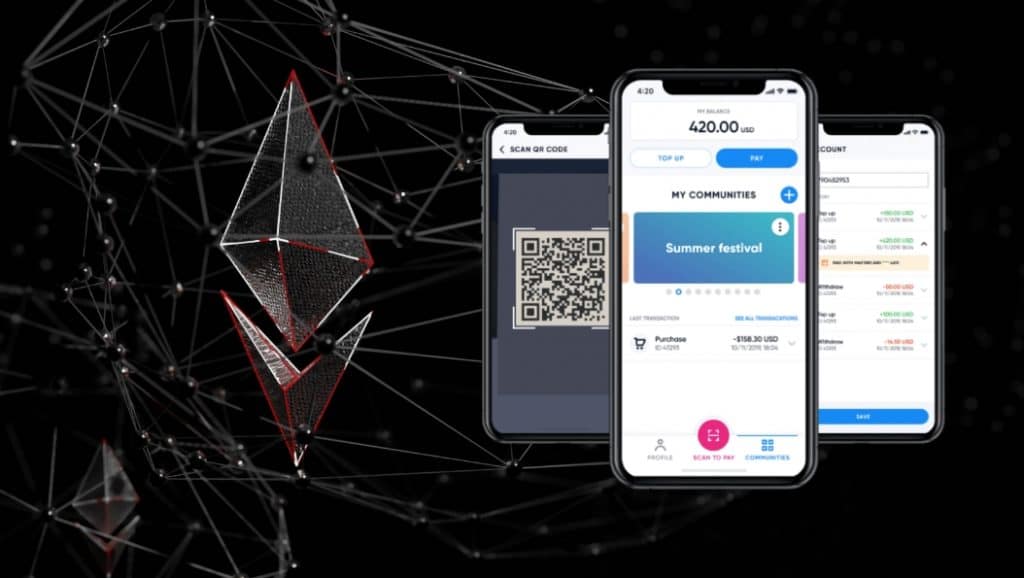

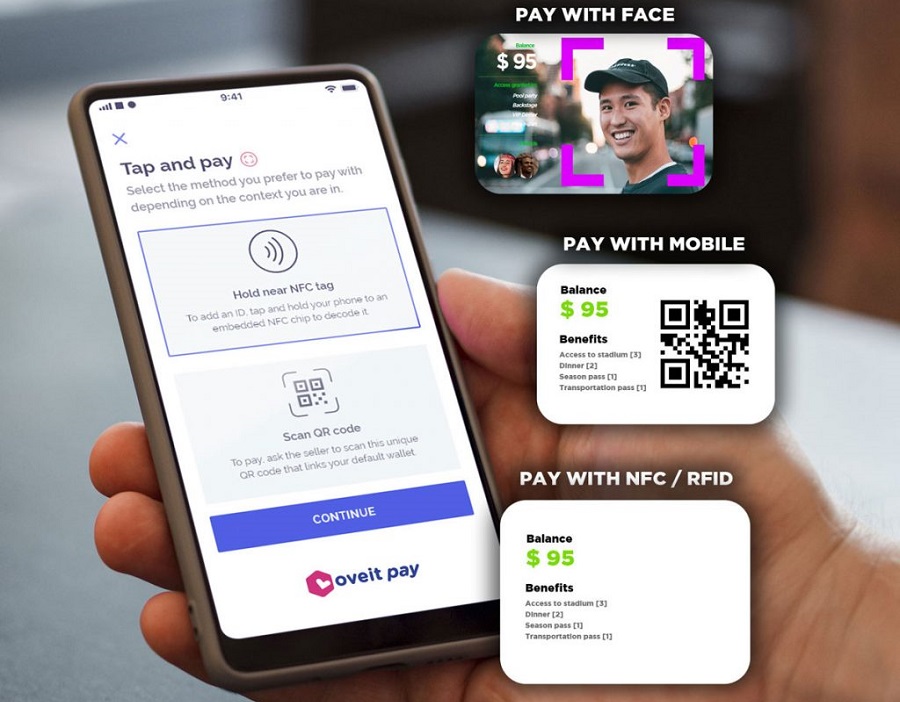

Oveit as a possible solution to track local recycling practices

Not long ago, we concluded that our technology can be utilized in different contexts. Among these, we feel that Oveit can be looked at as a viable solution to track and incentivize communities to recycle responsibly.

By using NFC wristbands or cards, community members can be rewarded and incentivized to recycle waste. It could add up gamification elements to an important cause. Participating locations can simply use any Android NFC enabled device to scan cards or wristbands. Based on the expected outcome, members can easily be rewarded in real-time. For instance, the economy owner might reward members that recycle at least three times per week. To record data, NFC readers could be placed nearby waste containers. Members that recycle enough are automatically rewarded and all that information is stored on their digital accounts (NFC wristband or card).